Here’s a sad reality: In order to raise a family in an expensive coastal city like San Francisco or New York, you’ve now got to make $350,000 or more a year.

You can certainly live on less, but it won’t be easy if your goal is to raise a family, save for your children’s education, save for your own home and save for retirement (so you can actually retire by a reasonable age).

A middle-class lifestyle is a reasonable ask. But thanks to inflation, it has gotten a lot more expensive if you want to have children. The median wealth of middle-income Americans has stayed flat for years, at about $87,140, according to the Federal Reserve’s latest Survey of Consumer Finances. Yet, prices for things such as housing and college tuition have risen tremendously.

In some major cities like San Francisco, the public school system starting in kindergarten is based on a lottery system, so even if you pay tens of thousands of dollars per year in property tax, your child is not guaranteed a spot in your neighborhood schools.

Coastal counties in the U.S. are home to almost half of the nation’s total population; therefore, this article is directly targeted at folks who need to live in these areas because of their jobs, schools or families.

Who makes $350,000 a year?

Before we look at how quickly $350,000 can be spent by a family of four, let’s go through a list of various workers who will eventually make around $350,000 on their own or in household income if they have a partner who also works:

- A Bay Area Rapid Transit janitor who makes $234,000 plus $36,000 in benefits marries a Bay Area Rapid Transit elevator technician who makes over $250,000 in salary and benefits. Together, they’d make well over $350,000.

- Starting total compensation packages for recent college graduate employees at Facebook, Google, Airbnb and Apple range from $120,000 to $150,000. By the time these employees turn 35, their total compensation alone can easily surpass $350,000.

- A 30-something first-year associate in investment banking earns, on average, a base salary of $150,000 plus a $20,000 to $100,000 bonus. After five years of experience, a total compensation of $350,000 should be achievable.

- A 20-something first-year big law associate makes a base salary of up to $190,000 plus a $20,000 signing bonus. By the end of their seventh year, many are making over $350,000.

- A 40-something tenured professor could make about $202,000 at the University of California, Berkeley, $260,000 at Columbia University and $218,000 at New York University.

- A specialist doctor finishing his or her fellowship at around the age of 32 could make about $300,000. After several years in the business, $350,000 isn’t unheard of.

The permutations of people making $350,000 goes on and on. For many professionals, if they aren’t there now, they’ll get to such a level of income eventually, especially if they team up with someone else.

Living a middle-class lifestyle on $350,000 a year

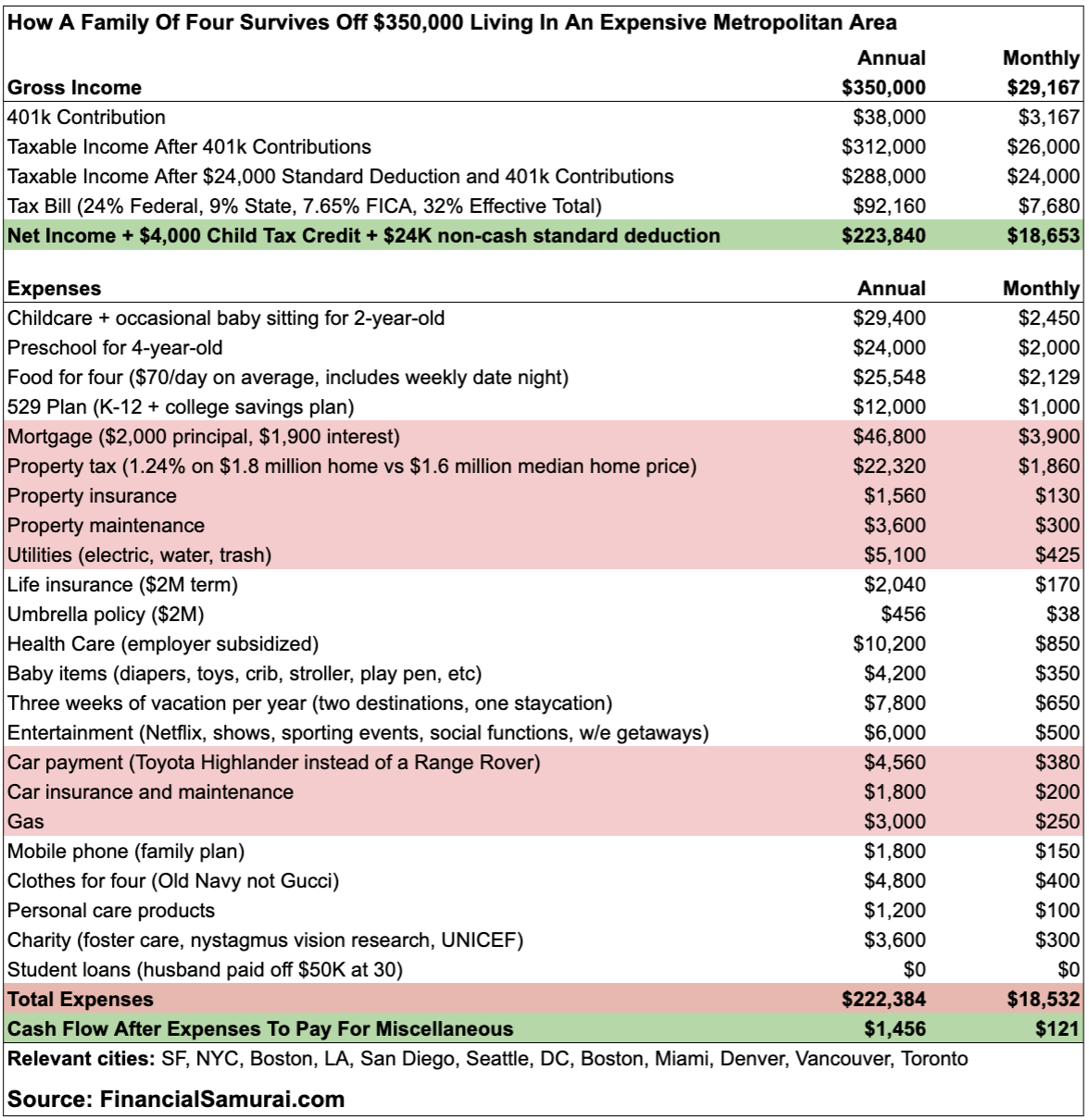

Below is an example budget of a dual-income household with two kids. The budget has been vetted by thousands of readers on my personal finance website, Financial Samurai, who also raise families in expensive cities like San Francisco, Los Angeles, New York, Boston and Washington, D.C.

Gross income review

In order to make $350,000 a year, both parents must be working. In this example, each parent puts away $19,000 in their respective 401(k)s for a combined $38,000 a year. After getting their standard $24,000 deduction, they pay $92,160 in total taxes and are left with $221,840.

Because this couple earns less than $400,000, they can receive a tax credit of $2,000 per child. Since they have two children, they get a $4,000 credit.

Expenses review

- Childcare: $2,450 per month. There’s no getting around this expense when both parents are working. Their childcare center costs $2,200 a month for full-time care. The couple then spends an extra $250 a month for some babysitting help.

- Preschool: $2,000 per month. The second child goes to preschool full-time. The $2,000 per month does not include the suggested $3,000 per child donation the school asks each year to help fund new construction. The parents’ ultimate plan is to send both children to private grade school, which costs about $35,000 from K-8 and about $45,000 from 9-12.

- Food: $2,129 per month. It makes little sense to spend hours cooking when you’re already tired and want to reserve your remaining energy for taking care of your kids. The budget includes expenses like groceries, eating out and food delivery.

- Mortgage: $3,900 per month. This amount isn’t bad for a $900,000 mortgage with a 3.25% interest rate; $2,000 out of the $3,900 goes toward paying down principal and building net worth. Therefore, this couple is adding $24,000 a year in forced savings to their annual 401(k) savings. (Their $1.8 million assessed house is a standard 2,200 square feet, four-bedroom, three-bathroom home on a 3,000 square foot lot. But it’s nothing fancy since the median price for a single-family home is $1.7 million in San Francisco. To give you an idea of how little you actually get for a $1.85 million home, below is an example of a typical home in that price range in Golden Gate Heights, one of San Francisco’s best-kept secret neighborhoods. As you can see, it’s a standard middle-class house — granted, with panoramic ocean views — and only has 1,288 square feet of living space, two bedrooms and one bathroom.)

- Property tax: $1,860 per month. The $10,000 SALT deduction cap for individuals and married couples hurts homeowners in expensive real estate markets. The annual property tax on a $1.8 million assessed house alone is roughly $22,320. On top of that, the couple is also paying about $25,000 in state income taxes. When you add on property tax, property maintenance and insurance, it costs this family over $75,000 a year in housing costs.

- Vacation: $7,800 per year. Three weeks of vacation a year is reasonable for the typical American household. After tax, four round-trip tickets to Hawaii will cost a family about $2,000. Then budget lodging for a week will cost at least another $1,400. There’s also food and activities to pay for. (No wonder why “staycations” are becoming more common for financially stretched households.)

- Car payment: $380 per month. When you have little ones, all you want to do is protect them from harm. Even if you consider yourself a good driver, one distracted driver reading a text message could cause a serious accident. No longer do you feel comfortable driving a compact city car while transporting your family. Instead, you want a vehicle with the highest safety rating.

- Baby/toddler things: $380 per month. You can spend as little or as much as you want on your baby. But this family buys disposable (not washable) diapers, tons of baby-proofing material, lots of educational toys, the best car seats and two strollers.

- Entertainment: $500 per month. Date night can easily cost $200 per outing for two once you include tickets to a ball game or an Off-Broadway show and transportation. Entertainment costs also include sporting equipment, memberships, Netflix, cable, internet and more.

- College savings: $1,000 per month. According to the College Board, the average cost of tuition and fees for the 2018-2019 school year was $10,230 for state residents at public colleges and $26,290 for out-of-state students. The average private school tuition is over $35,000. In 16 to 18 years, tuition will likely be double today’s averages.

Final cash flow review

The end result is annual cash flow of only $1,456, which could get spent in a hurry, as unexpected situations will likely pop up. Despite such little cash flow, this household is building roughly $63,000 in liquid net worth each year by paying down their mortgage and contributing to their employer-sponsored retirement accounts.

We all deserve to live a middle-class lifestyle. Unfortunately, we’ve first got to sacrifice more than ever to get there today.

Unfortunately, despite making $350,000 a year, this couple will be unable to retire before 60 because they aren’t building an after-tax investment portfolio to generate passive income. They can’t withdraw from their 401(k)s before age 59½ without a 10% early distribution penalty, nor can they rent out their home for income, given it’s their primary residence.

In order for this couple to achieve financial independence, they need to accumulate a net worth equal to at least 25 times their annual expenses — or 20 times their annual gross income.

In other words, they need to amass a net worth of between $5.5 million to $7 million if their income and expenses remain unchanged. That’s tough to do with so little in savings per year.

Recommendations for a better life

If you’re one of the many families struggling to get ahead in an expensive city on a high salary, here are five suggestions:

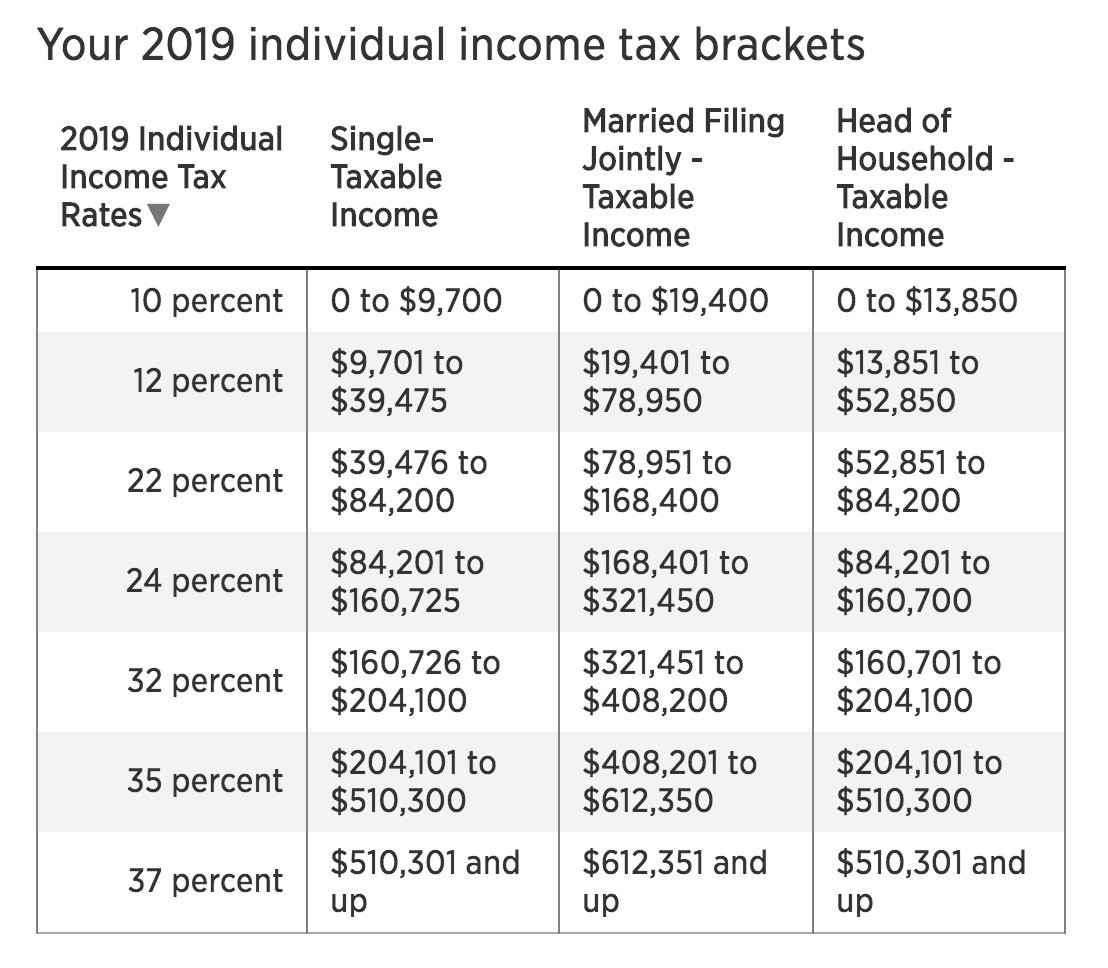

1. Limit your household income up to $321,451 after all deductions. A married couple can earn up to $321,451 and pay a 24% marginal federal income tax rate. Any dollar after $321,451 is taxed 8% higher at a 32% marginal federal income tax rate.

If you’re feeling overly stressed at work and want to spend more time with your children, consider working less if you’re making more than the 24% marginal tax bracket income threshold. Not only might your stress decline, you’ll be able to reduce childcare expenses.

2. Stop wanting a middle-class lifestyle. It’s worth sacrificing your lifestyle in the short term for long-term gain. By renting a more modest home for $4,000 a month, this family will free up $27,000 a year in cash flow. By sending their oldest to public elementary school, this family will gain another $24,000 a year in cash flow. An additional $51,000 a year in cash flow is huge when coupled with $38,000 a year in 401(k) contributions.

This couple could also limit their vacations to more local destinations, and cut back on meal spending by doing more bulk cooking and focusing on simple foods.

3. Build an after-tax investment portfolio. Earning passive investment income is the key to financial freedom. Using conventional rules, you can’t live off your 401(k) or IRA until the age of 59½. (Here’s my ranking of the best passive income investments today, so you can retire sooner rather than later.)

4. Move somewhere else. Once you’ve accumulated enough capital, consider relocating to a lower-cost area. Thanks to technology, there’s a multi-decade demographic trend towards living in the heartland, where property prices and rents are much cheaper.

5. Know your finances inside out. The people who end up with financial problems are typically the ones who don’t stay on top of their finances each week. Ten years later, they finally wake up and wonder where all their money went.

In the past, an Excel spreadsheet was fine. Now, there are plenty of free financial tools out there to use to not only track your finances, but x-ray your investment portfolios for excessive fees and help keep you on track to reaching your retirement goals.

The sad truth

According to the U.S. Census Bureau, less than 5% of households earn $350,000 or more a year.

While $350,000 might sound like a lot of money, it’ll go quickly when you’re raising a family in an expensive city. We all deserve to live a middle-class lifestyle. Unfortunately, we’ve first got to sacrifice more than ever to get there today.

{kind=link}